Fraud rarely walks in wearing a trench coat and holding a smoking gun.

Most of the time, it shows up as a “miscellaneous expense.”

A missing receipt.

A credit card charge that does not quite make sense.

A financial report that looks clean, but feels wrong.

That is what makes financial fraud so dangerous. It does not always scream. Sometimes it whispers.

A recent Department of Justice case is a perfect example. A former CFO of a Chicago-area company’s subsidiary was convicted after evidence showed she used a company credit card for personal purchases, including luxury furniture, designer apparel, and other personal expenses. According to the DOJ, she concealed the activity by falsifying general ledger entries, deleting thousands of credit card charges from the expense system, and preparing false financial statements.

In detective terms?

The money was missing, but the paper trail had been staged.

And that is the part every business owner needs to understand. Fraud is not just about someone taking money. It is often about someone changing the story your financials are telling.

So how do you know if your financials have been tampered with?

You start looking for clues.

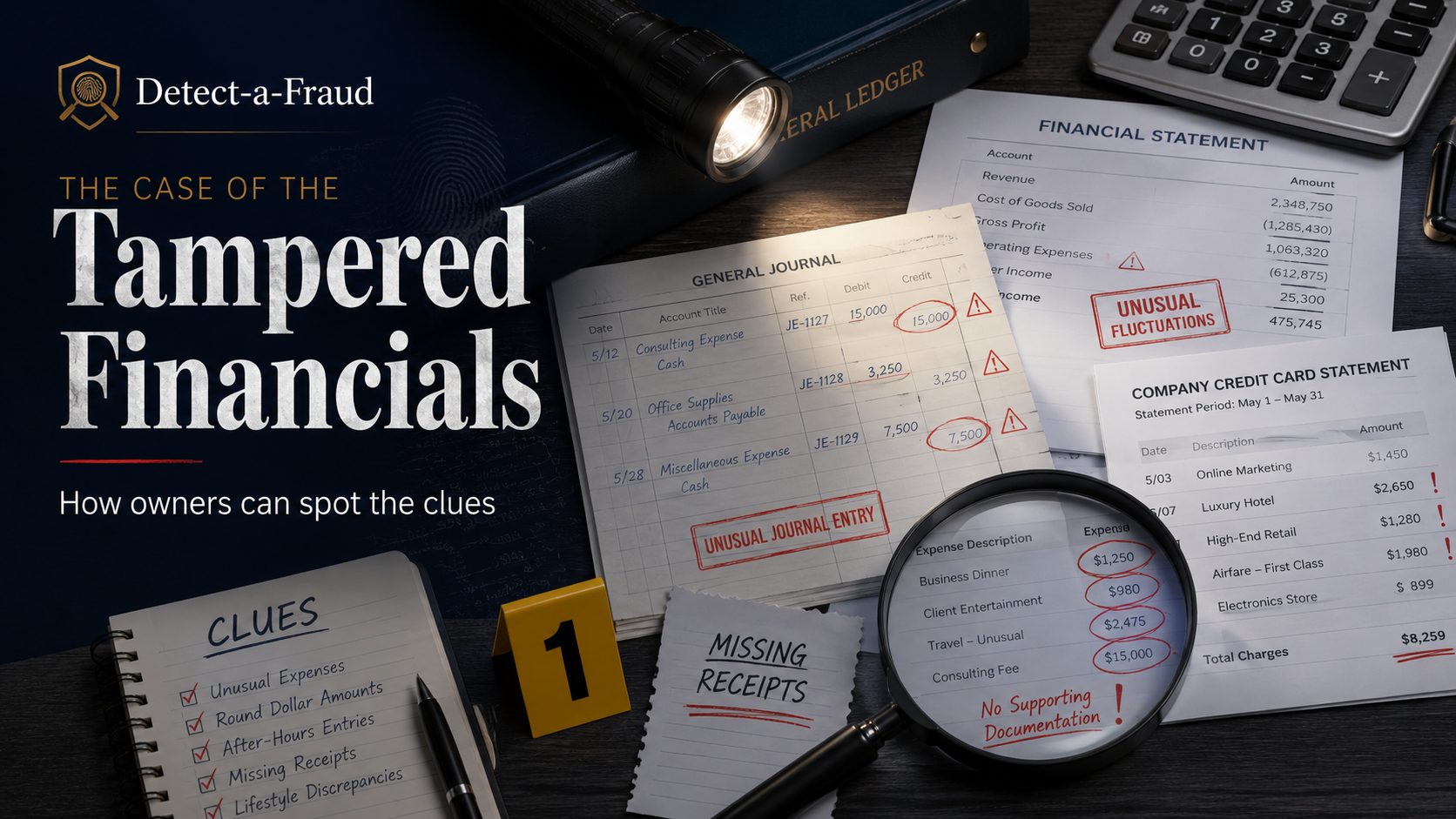

Clue #1: Expenses are hiding in plain sight

One of the oldest tricks in the fraud playbook is simple: bury the evidence.

A personal purchase may be coded as office supplies.

A questionable credit card charge may land in meals.

A luxury item may be tucked into “miscellaneous.”

A reimbursement may show up with no clear explanation.

On the surface, the books still balance. But balance does not mean truth.

Here is the owner question: does this expense make sense for the business?

If your numbers show a sudden spike in supplies, consulting, software, meals, travel, or miscellaneous expenses, do not just accept the category. Ask what is inside it.

Fraud loves vague categories because vague categories do not ask questions.

Clue #2: The receipts have vanished

Receipts are not just paperwork. They are evidence.

When receipts are missing, incomplete, altered, or repeatedly “coming later,” you have a trail problem.

A single missing receipt? That happens.

A pattern of missing receipts? That is a clue.

Especially with company credit cards, every charge should answer three basic questions:

What was purchased?

Who approved it?

Why was it for the business?

If no one can answer those questions clearly, the transaction deserves a closer look.

And if charges are being deleted from an expense system, that is not a bookkeeping hiccup. That is someone tampering with the evidence locker.

Clue #3: The general ledger tells a different story

The general ledger is where the real clues live.

Financial statements are the summary. The general ledger is the case file.

If someone is manipulating the financials, they may use journal entries to move amounts around, hide personal expenses, smooth out inconsistencies, or make the reports look better than reality.

Pay special attention to journal entries that:

Move expenses into vague accounts

Hit cash, credit cards, loans, payroll, or owner distributions

Are posted at month-end or year-end

Have no explanation

Have no supporting documentation

Are created and approved by the same person

A journal entry should explain what happened. It should not create more questions than answers.

If the entry looks like financial duct tape, pull on it.

Clue #4: The reports look clean, but cash feels tight

This is where owners need to trust their instincts.

If the profit and loss says the business is doing well, but you are constantly wondering where the cash went, stop and investigate.

Now, profit and cash are not the same thing. There are legitimate reasons they differ, including loan payments, accounts receivable, owner draws, prepaid expenses, and timing.

But the difference should be explainable.

If no one can walk you from profit to cash in plain English, you may not have a cash flow problem. You may have a reporting problem.

And sometimes, a reporting problem is where the fraud starts to surface.

Clue #5: The financials are a little too perfect

This may sound strange, but manipulated financials can look beautifully organized.

Too organized.

Expenses may stay oddly consistent. Profit margins may look smoother than the business actually feels. Reports may arrive polished, summarized, and conveniently light on detail.

That is not proof of fraud.

But it is a reason to ask better questions.

Real businesses are messy. Vendors change. Payroll moves. Client payments lag. Unexpected expenses pop up. If your reports look like a showroom while the business feels like a construction site, something may not be lining up.

Clean books are good.

Books that are “clean” because someone removed the inconvenient details? That is a problem.

Clue #6: Source documents do not match the reports

Every financial report should be traceable back to source documents.

The bank balance should match the bank statement.

Credit card activity should match the credit card statement.

Payroll should match payroll reports.

Vendor payments should match invoices.

Customer payments should match deposits.

If the report says one thing and the source documents say another, you have found a clue worth following.

This is where owners get into trouble. They review the finished report but never compare it to the source.

That is like reading the detective’s conclusion without looking at the evidence.

Clue #7: Deleted, voided, or changed transactions keep appearing

Fraud often leaves fingerprints in the audit log.

Deleted transactions.

Voided checks.

Edited entries.

Changed payees.

Reclassified expenses.

Prior-period adjustments.

Some of these may be perfectly legitimate. Mistakes happen. Corrections happen.

But patterns matter.

If transactions are constantly being changed after reports are finalized, ask:

Who changed it?

When was it changed?

Why was it changed?

What support proves the change was valid?

Your accounting system’s audit log is not just a technical feature. It is a witness.

Listen to it.

Clue #8: One person controls the entire money trail

This is one of the biggest risks in any business.

One person enters the bills.

That same person pays the bills.

That same person reconciles the bank account.

That same person manages the credit card.

That same person prepares the financial statements.

That is not efficiency. That is exposure.

And here is the part owners do not love hearing: the risk is often highest with the person you trust the most.

Not because they are automatically dishonest. Because trust without controls creates opportunity.

A strong financial system does not say, “I do not trust you.”

It says, “This business matters enough to protect.”

Clue #9: Questions make people defensive

A good financial professional should be able to explain the numbers.

Not with jargon. Not with attitude. Not with “you would not understand.”

Plain English.

If someone gets defensive every time you ask for backup, documentation, or a walkthrough, pay attention.

Watch for phrases like:

“That is too complicated.”

“You do not need to worry about that.”

“I already handled it.”

“We have always done it this way.”

“I will send it later,” followed by silence.

Questions are not accusations. Questions are internal controls.

And owners are allowed to ask them.

Clue #10: The story does not make sense

At the end of the day, financials tell a story.

They tell you where the money came from, where it went, what the business earned, what it owes, and what is left.

If the story does not make sense, do not ignore that.

Maybe revenue is up, but cash is down.

Maybe expenses are flat, but credit card balances are climbing.

Maybe payroll looks normal, but margins are shrinking.

Maybe the financials say everything is fine, but your gut says otherwise.

That gut feeling is not evidence, but it is a reason to start collecting evidence.

What should an owner do when something feels off?

Do not storm into the office making accusations.

That may feel satisfying for about ten seconds, but it can create legal, HR, and evidence problems fast.

Instead, slow down and preserve the trail.

Start here:

Pull bank and credit card statements directly from the financial institutions.

Compare those statements to the accounting records.

Review credit card charges for personal-looking expenses.

Look at journal entries for the last 12 to 24 months.

Check deleted, voided, and edited transactions.

Review user permissions in the accounting system.

Ask for support on unusual or vague transactions.

Bring in an outside professional if the answers are unclear.

You are not trying to be dramatic. You are trying to be responsible.

Because when the numbers have been tampered with, every day you wait gives the fraud more time to hide.

For law firm owners, the stakes are even higher

For law firms, financial tampering is not just a business issue. It can become an ethics issue.

If operating expenses are manipulated, that is serious.

If trust account activity is manipulated, that can put client funds and a law license at risk.

That is why law firm owners need financial systems that are not just accurate, but reviewable. The goal is not to hope everything is fine. The goal is to know.

You should be able to see:

What cleared the trust account

What client matter it belonged to

Who authorized the transaction

Whether the trust ledger matches the bank

Whether reconciliations were completed on time

Whether anyone changed prior-period activity

Hope is not a control. Review is.

The case takeaway

Fraud does not usually begin with a million-dollar theft.

It begins with access.

Then opportunity.

Then weak review.

Then small transactions no one questions.

Then bigger transactions hidden in plain sight.

By the time the owner realizes something is wrong, the fraudster may have already rewritten the financial story.

That is why owners need to think like investigators.

Not paranoid. Prepared.

Not accusatory. Curious.

Not buried in every transaction. But close enough to spot when the story stops making sense.

Your next move

Pick one month. Just one.

Pull the credit card statement directly from the bank. Then compare it to the accounting records.

Look for missing receipts, vague descriptions, personal-looking purchases, unusual categories, deleted transactions, and anything that makes you say, “Wait, what is this?”

That question, “Wait, what is this?” is often where the case starts.

And the sooner you ask it, the better chance you have of protecting your business, your cash, and your peace of mind.