She was 81.

That is the detail that makes people stop scrolling.

An 81-year-old former finance director in Kingston, Tennessee pleaded guilty after investigators found she had overpaid herself more than $131,000 in unearned salary and benefits.

And yes, that detail is surprising.

But here is the part business owners should pay attention to: this was not some flashy fraud scheme with fake vendors, offshore accounts, or a Hollywood-style money trail.

This was payroll.

Vacation time.

Sick leave.

Benefits.

Retirement calculations.

The boring stuff.

And that is exactly why it matters.

Fraud does not always walk in wearing a ski mask. Sometimes it sits at the payroll desk, knows the system better than anyone else, and has been trusted for so long that nobody thinks to ask, “Wait. Who is checking this?”

The suspect was not age. The suspect was access.

It is easy to get distracted by the age.

“She was 81!”

I get it. That is not what most people picture when they think of theft.

But fraud is not about age. It is about opportunity.

If one person can enter payroll, adjust leave balances, approve changes, process payments, and explain away the numbers, you do not have a payroll process. You have a trust exercise.

And trust is not an internal control.

That sentence may sting a little, especially for small businesses.

Because in small companies, everyone wears twelve hats. The office manager handles payroll. The bookkeeper pays bills. The owner reviews cash when they have time, which means usually when something already feels wrong.

Sound familiar?

That is how little leaks become big losses.

How does something like this happen?

In this case, investigators found issues tied to salary, benefits, vacation leave, sick leave, and retirement reporting.

For a small business, the same type of fraud can show up in plain sight:

An employee adds extra hours to their paycheck.

A payroll administrator pays out vacation time that was never earned.

A manager gives themselves a bonus without proper approval.

A long-time employee changes their pay rate and nobody reviews the payroll register.

Someone cashes out sick time, PTO, or commissions using calculations nobody else understands.

The numbers may not look shocking at first. A few hundred dollars here. A benefit adjustment there. A “correction” in the next payroll run.

But fraud loves repetition.

One bad payroll run is a mistake.

Years of bad payroll runs? That is a crime scene.

The red flag: one person knew too much and controlled too much

Here is where business owners need to get honest.

Do you have one person who knows “how everything works” financially?

The person who understands payroll.

The person who knows the bank login.

The person who handles vendor payments.

The person who talks to the CPA.

The person who can explain every weird transaction in a way that sounds reasonable.

That person may be wonderful. They may be loyal. They may have helped you build the business.

But if no one is reviewing their work, your business has a blind spot.

And blind spots are where fraud parks the getaway car.

What small businesses should do now

You do not need a giant finance department to reduce payroll fraud.

You need simple, consistent controls that actually get done.

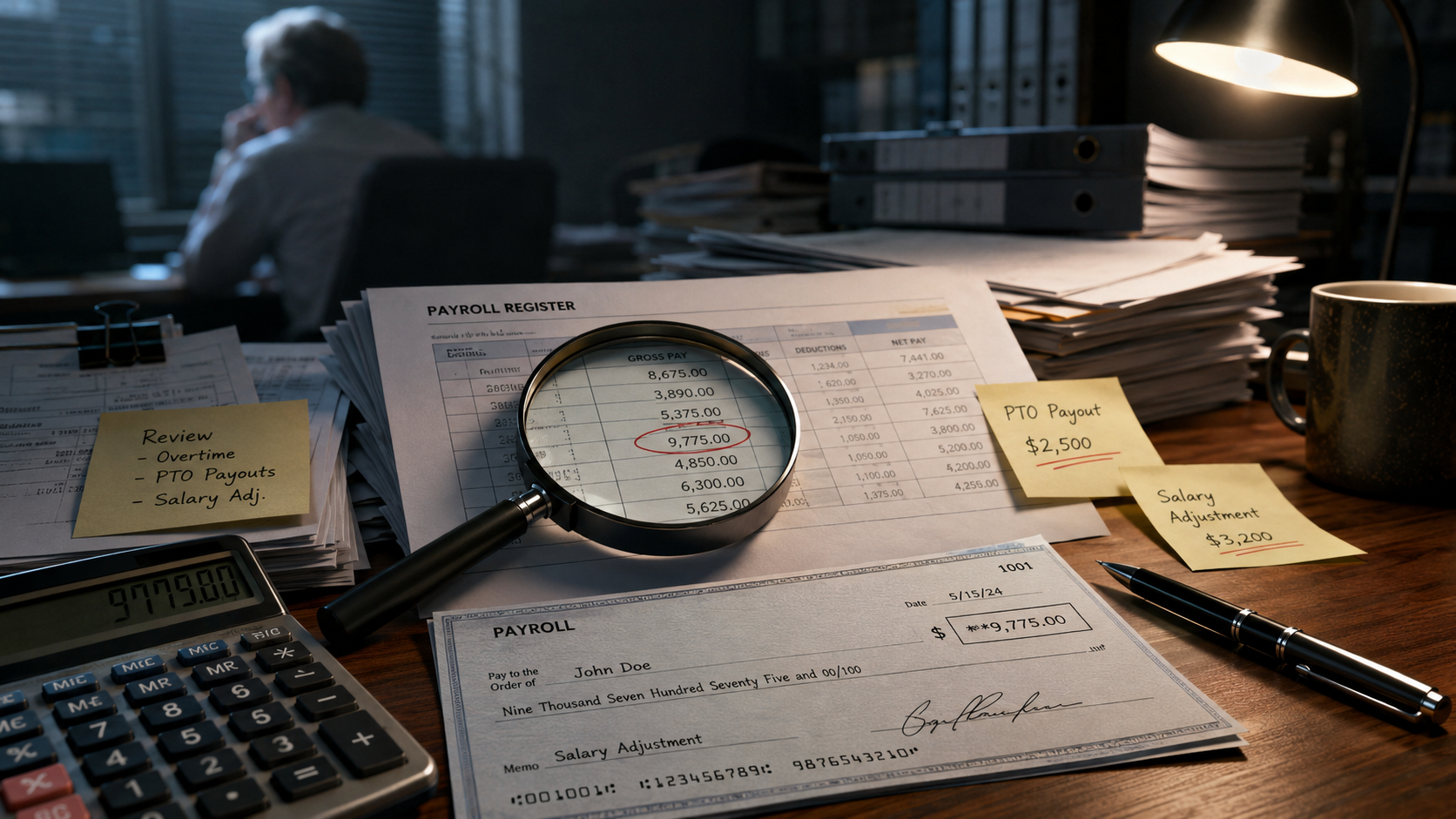

1. Review every payroll register before money goes out

Not after.

Before.

The owner or another approved reviewer should look at:

Employee names

Gross pay

Hourly rates

Salary amounts

Bonuses

Reimbursements

PTO payouts

Commission payments

Direct deposit changes

Ask yourself: “Does this payroll make sense based on who worked, who is salaried, who earned commissions, and who had approved PTO?”

This should take minutes, not hours. But skipping it can cost thousands.

2. Separate payroll entry from payroll approval

The person entering payroll should not be the only person approving it.

That does not mean you distrust them. It means you run a grown-up business.

One person prepares. Another person reviews. Then payroll is submitted.

Simple. Boring. Effective.

3. Lock down changes to pay rates and benefits

Pay rate changes should require written approval.

PTO cash-outs should require written approval.

Bonus payments should require written approval.

Direct deposit changes should require verification.

No “I thought we talked about it.”

No “I have always handled it this way.”

No “The system let me do it, so it must be fine.”

The system is not the boss. The approval process is.

4. Review leave balances regularly

Vacation and sick time balances can become a fraud hiding place.

If your system allows manual adjustments, someone should review those adjustments monthly or quarterly.

Look for:

Negative leave balances

Manual balance increases

Large cash-outs

Unusual corrections

Employees receiving leave payouts after termination or retirement

Adjustments made by the same person receiving the benefit

That last one is a big flashing red light.

5. Reconcile payroll to the general ledger

Payroll reports should agree to the books.

The amount processed through payroll should tie to payroll expense, payroll liabilities, and bank activity.

If the payroll report says one thing, the bank says another, and the books say a third thing, do not shrug and move on.

That is not an accounting annoyance. That is evidence.

6. Require owner-level review of retirement and benefit reporting

Retirement contributions, benefit deductions, employer matches, and taxable benefit reporting can be complicated.

That complexity makes them easier to manipulate.

At least once or twice a year, review compensation reported for retirement, benefits, and tax purposes. Make sure it matches approved pay.

This is especially important when someone retires, receives a payout, or has a compensation change.

7. Do not let long-term trust replace verification

The longer someone has been with your business, the more likely everyone assumes they are doing things correctly.

That is human nature.

It is also dangerous.

Fraud often happens where trust is highest and review is lowest.

A good employee will not be offended by controls. In fact, strong controls protect good employees from suspicion when something goes wrong.

The uncomfortable truth

Most payroll fraud does not happen because the owner is careless.

It happens because the owner is busy.

You are serving customers. Managing employees. Chasing sales. Putting out fires.

Meanwhile, payroll feels like one of those things that “just gets handled.”

Until it does not.

And by the time you find out, the money may be gone, the records may be messy, and the person responsible may have already retired, resigned, or moved on.

That is why fraud prevention has to happen before you feel suspicious.

Not after.

The detective’s takeaway

This case is not really about an 81-year-old woman.

It is about what happens when one person has too much control, too little oversight, and years of opportunity.

So here is the question for your business:

If someone changed their own pay, inflated their PTO, or paid themselves an extra benefit this month, would anyone catch it before the money left the bank?

If the answer is “I think so,” that is not good enough.

Pull the last payroll register. Review the pay rates. Look at PTO payouts. Check who can make payroll changes. Then decide what needs to change before the next payroll run.

Fraud prevention does not have to be fancy.

It just has to be done.