Synthetic identity fraud is getting more attention in auto finance right now, and for good reason. A recent Snell & Wilmer article called it one of the most costly and difficult-to-detect threats in auto lending, especially because fraudsters can combine real and fake personal information to create an entirely new “person” who does not actually exist. That synthetic identity can build credit, qualify for financing, and then disappear when the debt goes bad.

That sounds like an auto finance problem.

It is not.

Auto lenders may be a popular target because their transactions move fast, dealerships are under pressure to close, and financing decisions often rely heavily on credit bureau data. But the same fraud pattern can show up anywhere a business extends trust before it has fully verified who it is dealing with.

That includes lenders, landlords, vendors, employers, insurers, professional service firms, nonprofits, and yes, even law firms.

What Is Synthetic Identity Fraud?

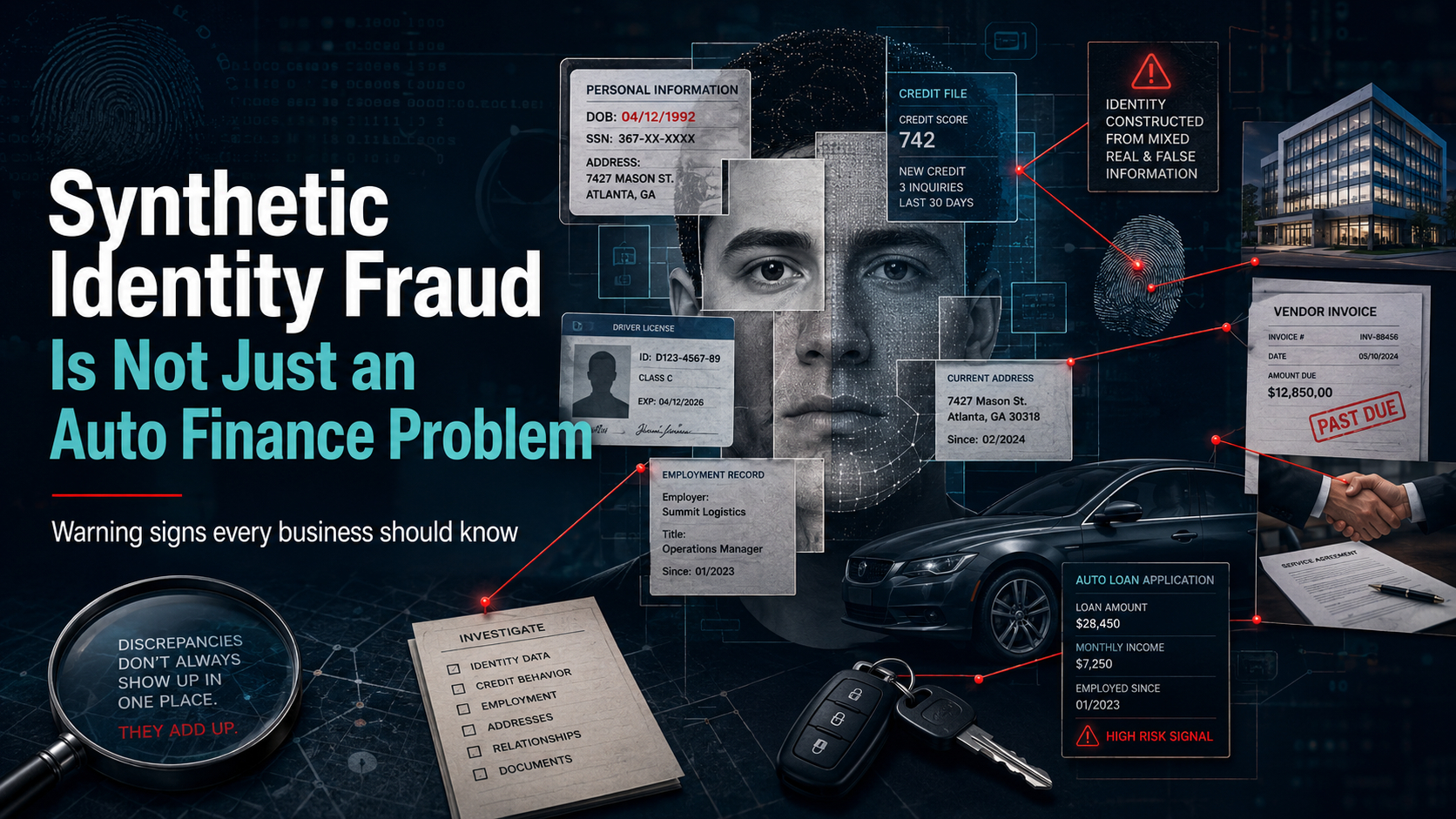

Synthetic identity fraud happens when someone pieces together real and fake information to create a new identity.

Think of it like a financial Frankenstein.

A fraudster might use a real Social Security number, often belonging to a child, a deceased person, or someone who does not actively monitor their credit, then attach it to a fake name, fake date of birth, fake address, fake email, and fake phone number. Over time, that identity may start to look legitimate.

The scary part? The identity may not trigger the same alarms as traditional identity theft because there may not be a real adult victim calling the bank saying, “That account is not mine.”

Instead, the synthetic identity slowly builds credibility.

A small credit account here. A payment history there. A thin credit file that starts looking stronger. Then, once the identity is “seasoned,” the fraudster goes after something bigger.

In auto finance, that might be a vehicle loan.

In another industry, it might be a business line of credit, vendor account, rental agreement, insurance policy, payroll record, grant application, or professional services engagement.

The Federal Reserve has described synthetic identity fraud as the use of a combination of real and fictitious personally identifiable information to fabricate a person or entity for financial gain, and has noted that it can escape traditional identity verification and credit screening processes.

Why Auto Finance Is a Warning Sign for Everyone Else

Auto finance is attractive to fraudsters because of speed, volume, and pressure.

Sound familiar?

Any industry with a fast-moving intake process can become vulnerable. When the focus is “get the deal done,” “onboard the client,” “approve the application,” or “process the payment,” fraudsters know there may be gaps.

The Snell & Wilmer article points to several auto finance risk factors, including online applications, remote identity verification, multiple applications across lenders, and reliance on credit bureau information.

Now translate that outside auto finance.

A nonprofit receives a vendor setup form by email.

A business hires a remote contractor.

A lender approves a small credit line based on clean-looking documentation.

A law firm accepts a new client who seems legitimate and urgent.

A company opens a customer account after reviewing documents that appear consistent on the surface.

Here is the problem: fraudsters are patient. They do not always go for the biggest theft on day one. Sometimes they build the story first.

And that is what makes synthetic identity fraud so dangerous.

Warning Signs Businesses Should Watch For

The red flags are often small. None of them prove fraud by themselves, but together they can tell a story.

Watch for:

Thin but surprisingly strong credit history.

A file that looks new, but has a score or credit profile that seems better than expected, deserves a second look.

Identity details that do not line up.

A Social Security number, date of birth, address history, phone number, or email address may not match the overall profile.

Multiple applications tied to the same contact information.

The same phone number, email address, mailing address, IP address, device, or bank account showing up across unrelated people or businesses is a major clue.

No meaningful digital footprint.

Not everyone lives online, but when someone claims to have a long professional or business history and there is almost no trace of them, pause.

Unverifiable income, employment, or business activity.

If the documentation looks polished but cannot be independently confirmed, that is not comfort. That is a reason to dig deeper.

Rapid escalation.

A new customer, employee, vendor, or borrower starts small, then quickly requests larger credit, faster payment, higher limits, or exceptions to normal procedures.

That last one matters. Fraud often starts with a test transaction. The fraudster wants to see whether your controls are real or just words in a policy manual.

This Can Hit Businesses and Nonprofits Too

Synthetic identity fraud is not limited to consumer lending. The Federal Reserve has also warned about synthetic business fraud, where criminals create fake companies to access loans, credit, accounts, and other financial products. Businesses may be especially attractive because they can qualify for higher limits than individuals.

That should get every business owner’s attention.

A fake business can look legitimate on paper. It may have a registered entity, website, business email, tax identification number, invoices, references, and bank account. But when you start pulling the thread, the whole thing may unravel.

For nonprofits, the risk can show up in grant applications, donor restrictions, vendor payments, reimbursement requests, payroll setup, or program funding.

For professional service firms, it can show up in client intake, retainer payments, trust account activity, vendor onboarding, or employee hiring.

For law firms in particular, this matters because fraudsters love urgency. They love pressure. They love situations where someone says, “We need this handled today.”

That is exactly when controls get skipped.

The Real Lesson: Verification Cannot Be One and Done

A lot of organizations think fraud prevention means checking identification at the beginning.

That is outdated thinking.

Synthetic identities are designed to pass basic checks. They may have enough “real” information to look credible. That means businesses need layered verification, not just a checkbox.

The Snell & Wilmer article notes that commonly discussed mitigation approaches include enhanced identity verification, cross-channel monitoring, stronger validation of Social Security numbers and identity attributes, employee training, and ongoing monitoring to catch suspicious accounts before a larger loss occurs.

In plain English?

Do not just ask, “Did we get the paperwork?”

Ask:

Does the paperwork make sense?

Can we independently verify it?

Does this person or business behave like the profile they presented?

Are they asking us to move faster than our controls allow?

Have we seen this phone number, address, account, or email before?

Do the financial records support the story?

That is where fraud gets caught, not in one magic software tool, but in the gap between what someone says and what the records show.

Practical Steps to Reduce the Risk

Here is where to start.

1. Tighten intake procedures.

Whether it is a customer, client, borrower, vendor, donor, employee, or contractor, define what must be verified before the relationship moves forward.

2. Separate speed from approval.

Fast service is great. Fast approval without verification is expensive.

3. Train your team on patterns, not just policies.

People need to know what “off” looks like. A checklist helps, but judgment matters.

4. Watch for repeated data points.

The same email, phone, address, bank account, IP address, or device showing up repeatedly should trigger review.

5. Verify financial claims independently.

Do not rely only on documents provided by the applicant, customer, employee, or vendor. Confirm employment, income, business existence, ownership, banking details, and authorization through independent sources when the risk is high.

6. Monitor after onboarding.

Fraud does not always happen at the front door. Sometimes the first transaction is clean because it is bait.

7. Document exceptions.

If someone overrides the standard process, make them explain why. Exceptions are where fraud loves to hide.

The Bottom Line

Synthetic identity fraud is not just about fake people buying cars.

It is about fake credibility.

Fraudsters are learning how to build identities, businesses, and financial stories that look believable enough to get through rushed systems. The businesses that will get burned are the ones relying on surface-level documentation and gut feelings.

The businesses that will be harder to fool are the ones that slow down at the right moments, verify independently, train their teams, and follow the money.

Because fraud does not usually walk in wearing a mask.

It walks in with clean paperwork, a reasonable story, and just enough urgency to make you skip the step that would have caught it.

Next step: Review your intake, vendor setup, customer approval, and payment change procedures. Pick one area where your team is relying too heavily on “the documents looked fine,” and add one independent verification step this week. That one step could save you from a very expensive lesson.